Non-traditional securitisation: Whole business securitisation (WBS)

Introduction

In the last few decades, a wide range of assets have been securitised. In 1999, the London City Airport securitisation was completed in the form of a whole business securitisation (“WBS”). This was part of the emergence of WBS in the United Kingdom (“UK”) at the time when the government was privatising many of its businesses. Since then, WBS has continued to develop and is expected to grow faster than any other applications of securitisation.

What is WBS?

WBS is a type of securitisation where cash flows are derived not from any receivables or debts (such as mortgage loans), which are generally foreseeable, but from the entire range of operating revenues generated by a whole business, which are potentially future, contingent and unpredictable in nature. Even though there is no formula or standard which determines whether a business is suitable for WBS, businesses in WBS to date often historically generate stable and predictable cash flows.

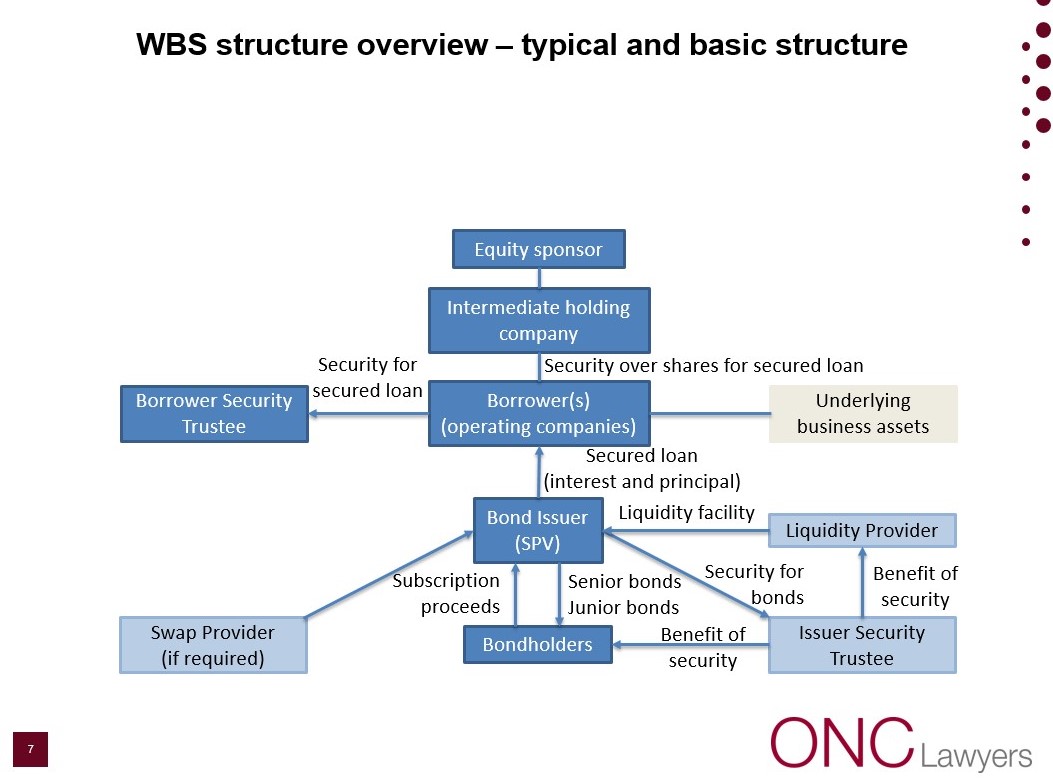

In the UK, WBS is generally structured as a hybrid of a standard securitisation and a secured corporate loan or bond mostly for convenience and simpler legal documentation and process. The secured loan structure must be robust enough so that, if the borrower goes insolvent, its operations can continue to be managed by the administrative receiver appointed by the investors with the view to repaying the debt over the remaining term of the securitisation. The secured loan is then being securitised to take advantage of the enhanced credit rating from tranching. A diagram of such a hybrid structure of WBS is shown below:

However, such a secured loan structure fails to take advantage of many other benefits afforded by a pure securitisation structure, including: (a) off-balance sheet treatment for assets and debt, (b) ring fencing of business assets from management, and (c) creation of new streams of revenues for the Borrower, and (d) cherry picking the most desirable business assets of the Borrower.

In contrast, in a pure securitisation model for WBS, the Borrower transfers the ownership of the desired business assets by way of assignment or novation to an SPV, who then appoints the Borrower as the initial operating manager, without the Borrower assuming an additional debt. As such, this structure avoids the drawbacks of the secured loan structure. A diagram of such a pure securitisation structure of WBS is shown below:

Advantages of WBS

WBS brings many of the benefits of traditional securitisations to business assets. For instance, WBS can result in more cost-effective financing, reduce dependence on bank credit, increase liquidity and improve accounting ratios.

Examples

WBS has been used as a means to finance companies owning a wide range of businesses, including hospitals, theatres and theme parks. Recent examples below involve WBS in the food and beverage industry, and leisure and entertainment industry.

Jack in the Box Inc.

Jack in the Box Inc. (“JIB”), a famous fast food chain in the United States, was successful in securitising a substantial part of its revenue-generating assets, such as its intellectual property, franchisee royalty streams, real estate and related company-owned restaurants in July 2019. The securitisation involved JIB issuing USD1.25 billion bonds. JIB used part of the proceeds from the WBS to repay its outstanding unrated debts. Credit rating agencies commented that JIB’s long operating history and developed franchise bases contributed to the success of the WBS.

Planet Fitness

Planet Fitness is a gym chain based in the United States. In March 2019, it completed its USD550 million WBS. Planet Fitness contributed substantially all of its revenue-generating assets, including existing and future domestic franchise, development agreements, vendor contracts, profits from domestic corporate-owned stores, commission and franchise payments, and intellectual property. Proceeds from the transaction were used for general corporate purposes and transaction expenses. As a result of the WBS, the credit rating of the senior debt was raised to a rating of BBB.

Conclusion

Unlike conventional securitisation, bonds issued through WBS may include intangible, future, contingent and unpredictable assets and revenue streams. WBS may make available financing with a lower interest rate and longer maturity. In light of the increasingly challenging economic environment, businesses seeking cash injection may find WBS an attractive option. In particular, WBS may be a useful tool for companies in businesses such as restaurants, healthcare, transport and utilities.

For enquiries,

please feel free to contact us at: E: capital@onc.hk T:

(852) 2810 1212 19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong

Kong Important: The law and procedure on

this subject are very specialised and

complicated. This article is just a very general outline for reference and

cannot be relied upon as legal advice in any individual case. If any advice

or assistance is needed, please contact our solicitors. Published by ONC Lawyers © 2020

W: www.onc.hk F:

(852) 2804 6311