Introduction to the ISDA architecture

What is ISDA and what does ISDA do?

International Swaps and Derivatives Association, Inc. (“ISDA”) is the trade association representing leading participants in the international privately negotiated (over-the-counter, or OTC) derivatives markets. It is a not-for-profit corporation formed in 1985 with its headquarters at New York and currently has over 915 members from 69 countries. ISDA’s members include almost all the major derivatives dealers, non-dealing financial institutions, central banks, corporations, law firms and software providers, etc.

Structure of the ISDA Documentation

The main aims of ISDA are to reduce the risk and cost of derivatives, streamline the documents used in the derivative markets and encourage the growth of markets in different derivative products. The ultimate goal is to make the OTC derivative markets safe and efficient. As part of its aim of streamlining the documents used in the derivative markets, ISDA has published a vast library of documentation for the documenting of derivative transactions. The standard documents include the ISDA Master Agreement, a schedule to the ISDA Master Agreement, ISDA Confirmations, ISDA Definitions, credit support documents and novation agreements.

ISDA Master Agreement

The most recent version is the 2002 ISDA Master Agreement, which has modified the 1992 version. It is a pre-printed umbrella document designed for use on all types of OTC derivative transactions, which includes all the boilerplate provisions, subject to variation by the schedule to it. The ISDA Master Agreement is divided into two parts. The first part constitutes a standard set of non-commercial terms and conditions, including representations, undertakings, events of default, termination events, change of law provisions, transaction netting provisions, etc. The second part is the schedule which allows the parties to tailor the first part as needed and make certain commercial terms.

ISDA Confirmations and Definitions

Under section 9(e)(ii) of the 2002 ISDA Master Agreement, it is stated that the parties will enter into a confirmation as soon as practicable. The ISDA Confirmations supplement and form part of the ISDA Master Agreement. They are used to document economic terms of transactions, such as the parties, dates, considerations, payment obligations and mechanisms, administrative details, etc. Besides, as ISDA from time to time publishes standard definition booklets for particular financial products, including interest rate and currency derivatives, commodity derivatives, inflation derivatives, equity derivatives, credit derivatives and foreign exchange and currency option derivatives, those definitions are incorporated by reference in the ISDA Confirmations, thereby avoiding the need for detailed and complex definitions to be set out within the confirmation itself. The most commonly used definitions set out below are the credit, equity, and interest rate and currency derivatives definitions.

ISDA Credit Derivatives Definitions

Credit derivatives are derivative instruments that derive price and value from the credit risk inherent in the debt obligations and/or the creditworthiness of a third party (i.e. the reference entity). The ISDA Credit Definitions are the market standard definitions for credit derivative transactions and contain the building blocks for all credit derivative transactions. The most recent version is the 2014 ISDA Credit Derivatives Definitions.

ISDA Equity Derivatives Definitions

Equity derivatives are financial instruments that reference and offer economic exposure to the performance of an equity asset or other equity-related variable from which the instruments’ price or value is derived. The ISDA Equity Derivatives Definitions are designed to be used in connection with confirmations relating primarily to option transactions, forward transactions and equity swaps governed by an ISDA Master Agreement already entered into by the parties. The most recent version is the 2011 ISDA Equity Derivatives Definitions, which provide a framework of market-standard terminology and contingencies for when prices cannot be obtained, trading days for exchange operation or for the processing of calculations are disrupted, or underlying shares are nationalised or merged.

ISDA Definitions

Interest rate derivatives and currency derivatives are financial instruments with a value that is linked to the movements of interest rates and currency exchange rates respectively. The purpose of ISDA publishing the definitions relating to interest rate and currency derivatives is to provide a basic framework for the documentation of privately negotiated interest rate and currency derivative transactions. The most recent are the 2006 ISDA Definitions and ISDA is currently working with members to draft the 2020 version of these definitions.

Credit Support Documents

Derivatives trading carries high risks while OTC derivatives are even riskier than derivatives traded through exchanges. In order to reduce such risks, the parties generally provide collateral or security as credit support for their obligations under derivative transactions. The credit support documents can be either in the form of a credit support annex which forms part of the schedule to the ISDA Master Agreement, or in the form of a credit support deed which is a standalone document.

Conclusion

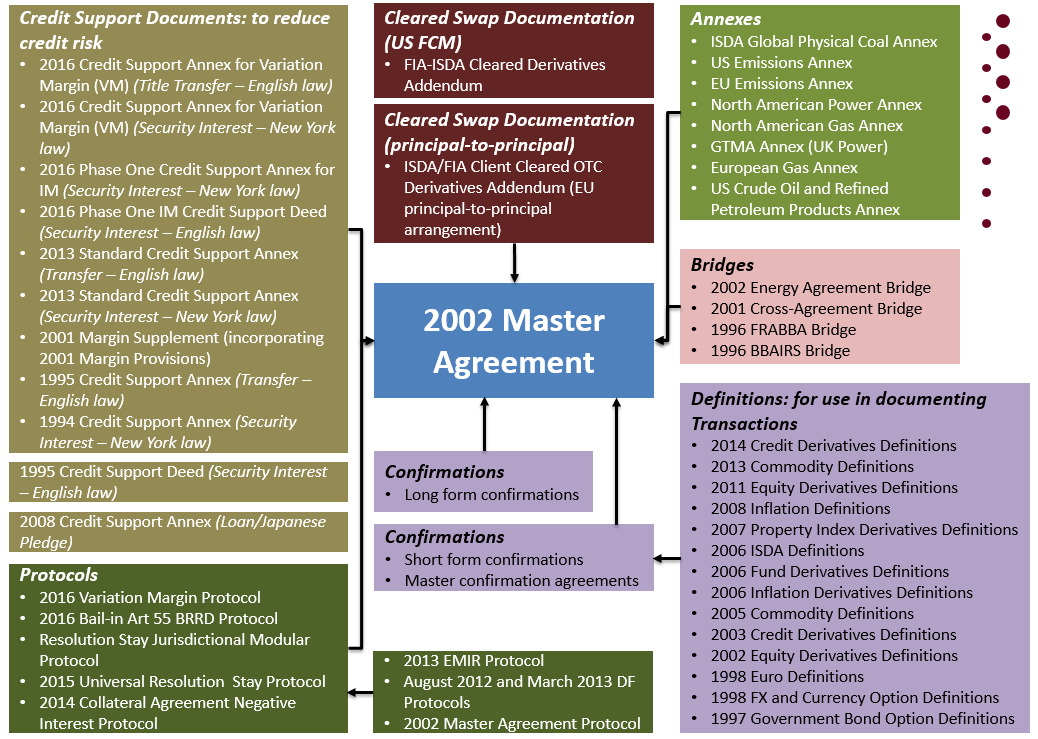

Thanks to ISDA, market participants are able to apply the set of standardised derivative transaction documentation for better collaboration and save time and resources for negotiation and risk management. Nonetheless, market participants still need to customise their own derivative transaction documents by varying certain provisions and adding commercial terms according to their business needs. We also set out below a diagram displaying a general overview of most of the ISDA documentation currently available to market participants.

For enquiries,

please feel free to contact us at: |

|

E: capital@onc.hk T:

(852) 2810 1212 19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong

Kong |

|

Important: The law and procedure on

this subject are very specialised and

complicated. This article is just a very general outline for reference and

cannot be relied upon as legal advice in any individual case. If any advice

or assistance is needed, please contact our solicitors. |

|

Published by ONC Lawyers © 2020 |