The HKEx Issues New Guidance on Trading Halts

Introduction

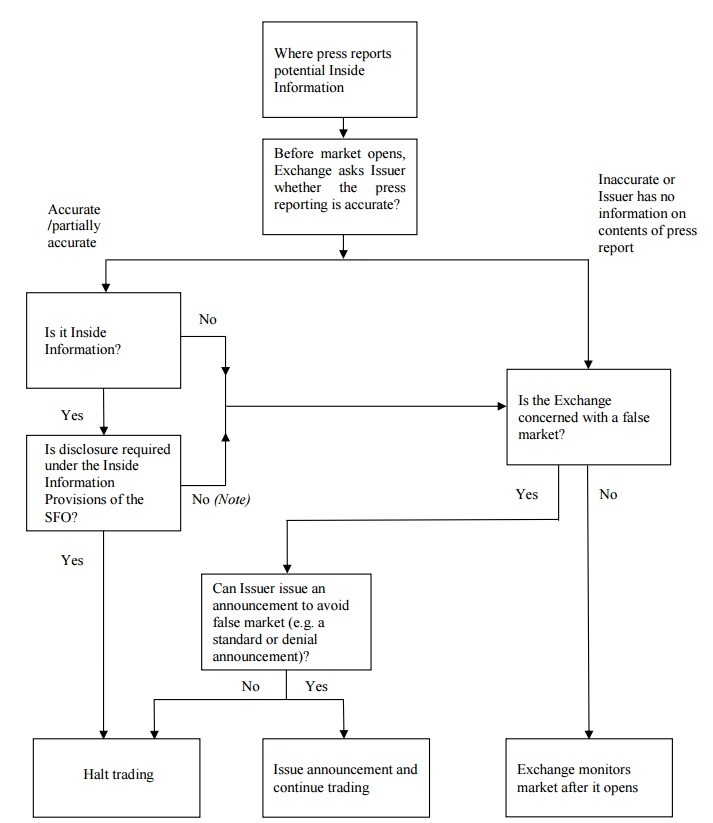

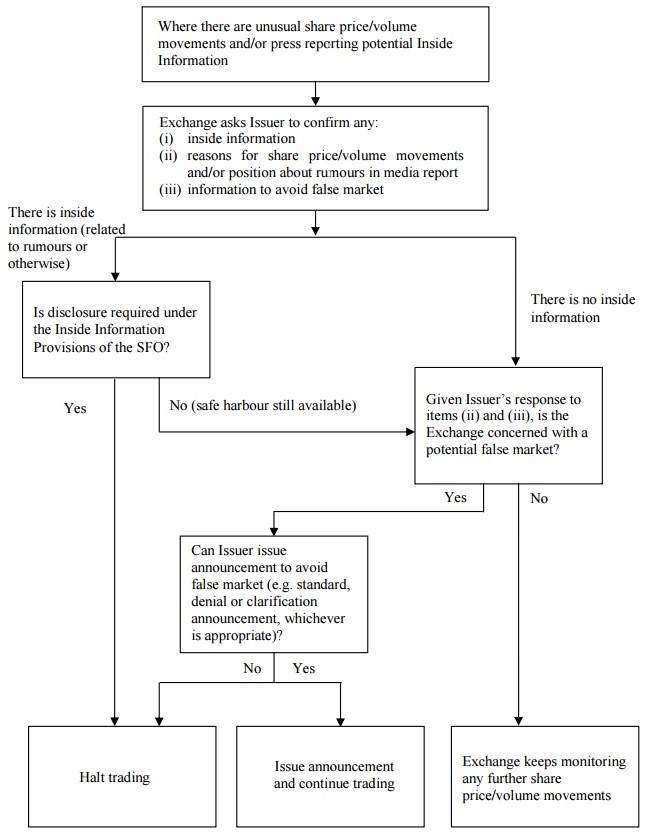

A trading halt is generally a temporary interruption in the trading of a security or group of securities in anticipation of or in reaction to an unusual event or condition affecting a security or group of securities. The purpose of it is to allow inside information to be adequately disseminated and assessed by the market, in order to protect investors and the general public. Recently, the Stock Exchange of Hong Kong (“HKEx”) has tightened up its practice of granting trading halts, limiting them to situations that the HKEx deems necessary to ensure investors are not denied reasonable access to the market. A guidance letter on trading halts (HKEx-GL83-15)(the “Guidance Letter”) has been published on 11 December 2015 to clarify this practice. Helpfully, the Guidance Letter also includes two diagrams on the decision flows that the HKEx will adopt when considering whether or not to grant a trading halt. These diagrams are included in the appendix to this newsletter.When is a Trading Halt Necessary?

Necessary?

Under Main Board Rule 13.10A and GEM Rule 17.11A, an issuer must voluntarily apply for a trading halt as soon as reasonably practicable in the following circumstances:

1. It has information which must be disclosed to avoid, in the opinion of the HKEx, a false market; or

2. It reasonably believes that there is Inside Information which must be disclosed under the Part XIVA of the Securities and Futures Ordinance (“SFO”); or

3. Circumstances exist where it reasonably believes or it is reasonably likely that confidentiality may have been lost in respect of certain Inside Information.

Guidance on Trading Halts Pending Disclosure of Material Information

Avoiding and Minimizing Halt

In the guidance letter, issuers are reminded to avoid and minimize trading halts by adhering to the following practices:

1. Issuers should plan their affairs so that a trading halt can be avoided and/or any halt can be kept as short as is reasonably possible;

2. Issuers should ensure that trading of their securities resume as soon as practicable following the publication of an announcement or when the reasons for the trading halt no longer apply (Main Board Rule 6.07; GEM Rule 9.09);

3. Issuers should sign significant agreements only outside, but not during, trading hours and prepare their announcements ahead of signing of agreements, such that the announcements can be released immediately after agreements are signed, since announcements containing Inside Information can only be published outside trading hours;

4. Issuers should seek early consultations with, or regulatory clearance from, the HKEx, in respect of complicated transactions for which announcements require pre-vetting by the HKEx, and such consultation should take place before the signing of a significant agreement to avoid/ minimize the duration of any trading halt;

5. Issuers should ensure that the information in transaction announcements is clearlypresented in plain language and contain information required under the Listing Rules and other applicable regulations, as unnecessary lengthy disclosures may result in delaying the release of the announcement and prolong the trading halt; and

6. Issuers should publish the announcement and resume trading as soon as possible, when trading is halted pending an announcement of a transaction.

Incomplete Proposals and Business Negotiations

Under Main Board Listing Rule 13.05 and GEM Rule 17.10, issuers have an obligation to comply with Part XIVA of the SFO to disclose Inside Information, and one commonly used safe harbour from such obligation to disclose Inside Information is the preservation of confidentiality of information concerning an incomplete proposal / business negotiation.

In this regard, issuers are reminded in the guidance letter to take effective and appropriate measures to preserve confidentiality of Inside Information. Examples of such measures include the use of code names in circulating draft documents among professional parties, and the execution of confidentiality undertakings. The HKEx made it clear that it would only agree to a trading halt if there appears to be a reasonable concern on the leakage of Inside Information and/ or practical difficulty in maintaining confidentiality.

Response to the HKEx’s Enquiries

Under Main Board Listing Rule 13.10 and GEM Rule 17.11, the HKEx may make enquirieson unusual movements in price or trading volume of issuer’s shares and issuers must respond promptly.

In the Guidance Letter, issuers are reminded that it is critically important that their authorized representatives are contactable at all times and are in a position to answer enquiries from the HKEx on any unusual share price and volume movements and media news. In particular, when replying the HKEx’s enquiries, the authorized representatives of the issuers are expected to confirm the following:-

1. whether the directors of the issuers are aware of any matter of development that is or may be relevant to the unusual trading movement of its listed securities, or information necessary to avoid a false market, or any Inside Information which needs to be disclosed under the announcement (Main Board Rule 13.10(2) and GEM Rule 17.11(2)); and

2. if so, provide details.

Besides, where issuers are engaged in confidential business negotiation, they should monitor their share prices and volume movements and media coverage. After receiving HKEx’s enquiries, they must promptly and carefully assess whether it has a disclosure obligation under the SFO to disclose Inside Information, if any. Issuers should have in place an appropriate delegation of authority to allow for timely release of information to the HKEx and to the public by publication of an announcement.

Handling of Specific Market Speculations and Negative Publicity

In relation to market specific rumours, speculations or negative publicity made by commentators, issuers’ directors must promptly and carefully assess whether a disclosure obligation arises under the SFO and/or the Listing Rules. If any market comment has, or is likely to have, an effect on the issuers’ share price or volume such that there may potentially be a false market, the HKEx may require the issuer to make a clarification announcement. Where an issuer is unable to make a clarification announcement in response to the HKEx’s requests promptly, the HKEx may require it to request a trading halt pending the clarification to address potential or actual false market. Therefore, issuers are reminded to establish procedures to actively monitor their share price and any news, comments, or reports relating to them circulated in the market.

Dual or Multiple Listings and A and H Share Issuers

Specific guidance for dual or multiple listings and A and H share issuers are provided in the Guidance Letter. Dual or multiple-listed issuers are reminded to ensure that simultaneous dissemination of information in the different markets and, if it is impracticable (e.g. due to time zone differences), that the information be disseminated before the market opens in HK. A and H share issuers are reminded that if they have unpublished material information warranting a trading halt in both markets, such trading halt requests should be made by the issuer with both exchanges simultaneously.

Administrative Matters

Last but not least, issuers are reminded that any application for trading halts should be made in writing before 9:00 a.m. for trading halt in the morning trading session and 1:00 p.m. for trading halt in the afternoon trading session.

Issuers must also release an announcement promptly after a trading halt is effected to inform the market of a reason for its trading halt. Listed issuers should also disclose details on the reason for the trading halt.

If a trading halt cannot be avoided and significant time is needed to prepare and release the relevant material information, listed companies should publish periodic updates on their progress towards preparing information disclosure and trading resumption.

Appendix

Diagram 1: Decision tree about whether a trading halt is appropriate where the HKEx detects a possible leakage of Inside Information before market opens

Diagram 2: Decision tree about whether a trading halt is appropriate where the Exchange detects a possible leakage of Inside Information during trading hours

For enquiries, please feel free to contact us at: |

E: cc@onc.hk T: (852) 2810 1212 19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong Kong |

Important: The law and procedure on this subject are very specialised and complicated. This article is just a very general outline for reference and cannot be relied upon as legal advice in any individual case. If any advice or assistance is needed, please contact our solicitors. |