The Basel III Framework on Liquidity Coverage: A Step Forward Towards a More Resilient Banking System

Background

The severe economic and financial crisis in 2007 (“Crisis”) was due to deterioration of the level and quality of the capital base, accompanied by excessive on and off-balance sheet leverage built up by the banking sectors of many jurisdictions. Many banks, despite adequate capital levels, still experienced difficulties because they did not manage their liquidity prudently. Following the rapid evaporation of liquidity, the banking system came under severe stress. As a result, central banks were forced to inject liquidity into banks. In response to this problem, the Basel Committee on Banking Supervision (“Basel Committee”), of which the Hong Kong Monetary Authority (“HKMA”) is a member, established regulatory frameworks for worldwide banking sectors. The Basel Committee issued the Basel III framework on regulatory capital and liquidity standards (“Basel III”) in December 2010.

This article will focus on the Basel III requirements on the liquidity.

Two Standards for Funding Liquidity

The Basel Committee has established two minimum standards for funding liquidity. These two standards are designed to achieve two separate, but complementary objectives. The first one, the Liquidity Coverage Ratio (“LCR”) was designed to promote short-term resilience of a bank’s liquidity profile by ensuring that it has sufficient high-quality liquid assets to survive a significant stress scenario lasting for a month. The second standard, the Net Stable Funding Ratio (“NSFR”) is designed to achieve long term resilience by having a time horizon over one year. This article will explore each of these standards in turn.

Liquidity Coverage Ratio

The LCR aims at ensuring that banks have a level of high quality liquid assets that can easily be converted into cash to satisfy liquidity needs within a 30 day time horizon should a significantly severe liquidity stress scenario arise. The LCR assumes that by the end of the 30 day period, appropriate measures will have been taken to resolve the problem.

The following LCR is only applicable to Category 1 Institution, which should meet the following criteria as set out in Part 1 of Schedule 1 of the Banking (Liquidity) Rules (Cap.155Q) (“BLR”):

1. The authorized institution is internationally active.

2. The authorized institution is significant to the general stability and effective working of the banking system in Hong Kong.

3. The liquidity risk associated with the authorized institution is material.

4. The authorized institution (first-mentioned institution) is so connected to another authorized institution (being a category 1 institution) (second-mentioned institution) that, if the first-mentioned institution were not designated as a category 1 institution, such connection would prejudice, or may potentially prejudice (a) the calculation of the LCR under Part 7 of the BLR by the second-mentioned institution; (b) the calculation of the liquidity maintenance ratio under Part 8 of the BLR by the first-mentioned institution; or (c) the calculation mentioned in both paragraphs (a) and (b).

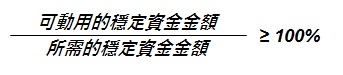

The LCR is calculated by the following formula:

This formula is built on traditional coverage ratios. The total net cash outflows for the formula are to be calculated for the next 30 days in the future. The standard itself requires that the value of the LCR be no lower than 100%. What this means, is that the current stock of high quality liquid assets must be capable of meeting the net cash outflow for the next 30 calendar days at the very least in the event of severe liquidity stress.

Numerator

The numerator is stock of high-quality liquid assets. Under the formula, banks are required to have a stock of high-quality liquid assets that are capable of covering total net cash outflows over a 30-day period in the aforementioned stress scenario. What constitute high-quality liquid assets, whilst there is no formal definition, include assets that:

· are of low credit and market risks,

· have ease and certainty of valuation,

· have low correlation with risky assets,

· are listed on a developed and recognized exchange market.

Liquid assets are also categorized in two types: level 1 and level 2.

Level 1 assets include cash, central bank reserves, marketable securities representing claims on or guaranteed by sovereigns, central banks, public sector entities, relevant international organisation or multilateral development bank, or that are Exchange Fund debt securities (including a 0% risk-weight under the Basel II standardized approach to credit risk), market debt securities that are issued by the sovereign or central bank in a currency that is not the local currency of that country (bearing a non-0% risk weight under the Basel II framework).

Level 2A assets include marketable securities representing claims on or guaranteed by sovereigns, central banks, public sector entities, or multilateral development banks that satisfy certain conditions (including a 20% risk-weight under the Basel II Standardized approach to credit risk); corporate debt securities (not issued by a financial institution or any of its affiliated entities (including a credit rating from a recognized external credit assessment institution (“ECAI”) of at least AA-); and covered bonds (not issued by the bank itself or any of its affiliated entities) that satisfy certain conditions (including credit rating from a recognized ECAI of at least AA-).

Level 2B assets comprise corporate debt securities with a 50% haircut, common equities with a 50% haircut, and residential mortgage-backed securities (“RMBS”) with a 25% haircut.

In the composition of a bank’s stock of high quality liquid assets, level 1 assets can comprise an unlimited portion, whereas level 2 assets may at most comprise 40% of the total stock. Level 2B assets should constitute no more than 15% of the stock of liquid assets after application of haircuts.

Denominator

The denominator is the total net cash outflows, which is given by the total expected cash outflows minus the total expected cash inflows in the specific stress scenario for the subsequent 30 calendar days (“LCR period”). This is illustrated by the following formula:

Total net cash outflows over the next 30 calendar days = outflows – inflows

Cash outflows include, inter alia, retail deposit run-off, debt securities issued by the institution redeemable during the LCR period, contingent funding obligations, unsecured wholesale funding run-off as well as secured funding run-off, liabilities arising from derivative contracts, potential drawdown of undrawn committed facilities, contractual lending obligations, contractual cash outflows.

Cash inflows shall include contractual cash inflows that are expected to be received within the LCR period, arise from assets that are fully performing and in respect of which the institution has no reason to expect a default within the LCR period, and under the assumption that those inflows are received by the institution at the latest possible date based on contractual rights available to its customers but shall not include any cash inflows that are contingent in nature.

Net Stable Funding Ratio

As mentioned, the NSFR is a year-long horizon, designed to promote better medium and long-term funding of the assets and activities of banks. It also aims at addressing liquidity mismatches and incentivising banks to use long-term funding. The standard is given by the following formula:

This formula is based on traditional net liquid asset and cash capital methodologies, and requires that the ratio of available stable funding (the numerator) to be greater than the amount of required stable funding (the denominator).

Numerator

The numerator is the available amount of stable funding. It concerns the most stable sources of funding to be regulatory capital, funding which has a maturity of at least 1 year and deposits. However, for the purposes of the NSFR, extended borrowing from central bank lending facilities that are outside regular open market operations are not considered in order to prevent reliance on central banks as a source of funding.

Denominator

The denominator is the required amount of stable funding. Examples are loans to financial institutions, assets which are encumbered for a period of one year or more, net amounts receivable under derivative trades and fixed assets.

It is expected that more elaborated guidelines in respect of the implementation of NSFR will be laid down by the HKMA before its full implementation in 2019.

Implementation Timetable

The HKMA is committed to implementing the Basel III framework in accordance with the timetable proposed by the Basel Committee. Under this timetable, implementation of the liquidity ratios began on 1 January 2015 in phases, with the starting minimum ratio requirement at 60%, increase of 10 percentage point per annum, and full implementation from 1 January 2019.

The above details in relation to the LCR and the NSFR are only a brief introduction of the relevant rules. For further details, you are advised to refer to the BLR and further guidelines to be laid down by the HKMA.

For enquiries, please contact our Corporate & Commercial Department:

E: cc@onc.hk

T: (852) 2810 1212

W: www.onc.hk

F: (852) 2804 6311

19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong Kong

Important: The law and procedure on this subject are very specialised and complicated. This article is just a very general outline for reference and cannot be relied upon as legal advice in any individual case. If any advice or assistance is needed, please contact our solicitors.