Listing of a PRC Business - Red Chip Listing Breakthrough

Introduction

Planning, executing, and managing an initial public offering (“IPO”) of People’s Republic of China (“PRC”) businesses is a challenging task, especially for fulfilment of the harsh regulatory requirements. Following the introduction of “Regulations Concerning the Merger and Acquisition of Domestic Enterprises by Foreign Investors” (commonly known as “Circular 10”) in 2006, the listing process for red chip enterprises has become more complicated. However, in past years, we have witnessed various ingenious reorganisation plans adopted by different PRC enterprises to oust the application of Circular 10 on their listings in Hong Kong. Some of the common plans are summarised in this newsletter.

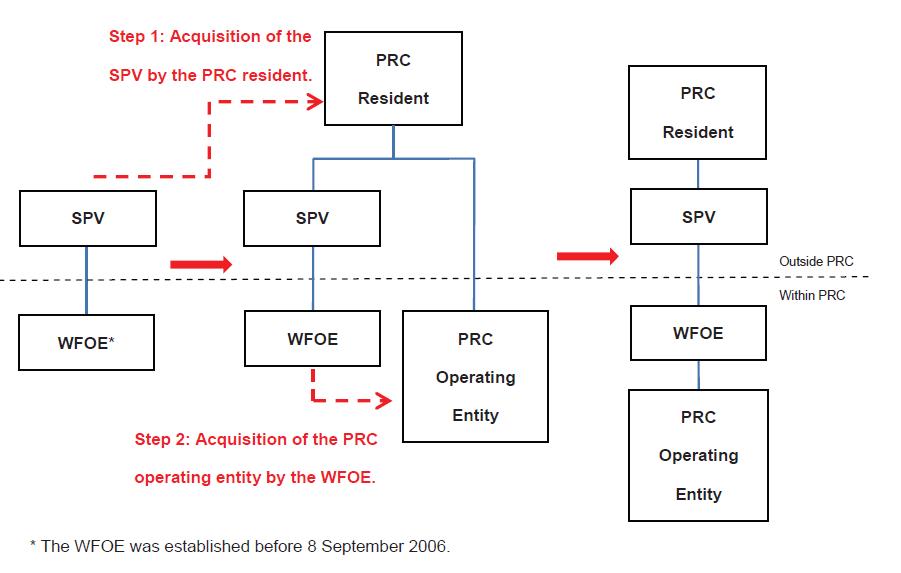

Acquisition of red chip structures established prior to 8 September 2006

PRC lawyers generally consider that red chip structures established prior to 8 September 2006 were not caught by Circular 10. Hence, after the implementation of Circular 10, many PRC enterprises with red chip structures established prior to 8 September 2006 continued with their listings in Hong Kong. For those without such red chip structures, they might acquire an offshore special purpose vehicle (“SPV”) with an existing red chip structure (usually comprising a wholly foreign-owned enterprise (“WFOE”)) owned by third parties.

A diagram summarising the key reorganisation steps involved is set out below for illustrative purposes:

As Circular 10 has been implemented for more than 8 years, it has become more and more difficult to find offshore SPVs with red chip structures established before 8 September 2006 and are available for acquisition.

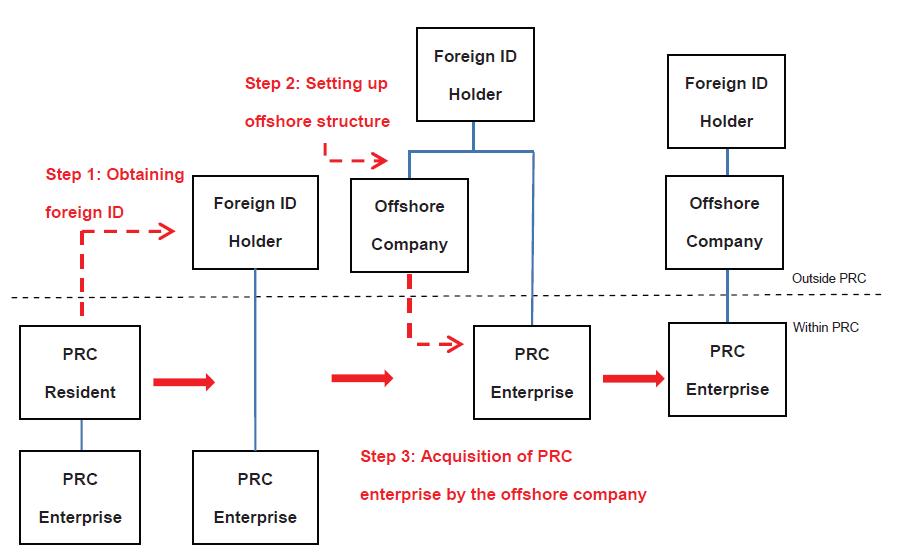

Obtaining foreign identity by the PRC business owner

Many PRC lawyers consider that PRC business owners who have obtained foreign identities are not subject to Circular 10. Hence, some PRC business owners achieve their listing plans by obtaining foreign identities from countries offering citizenship in return for investment, such as Saint Kitts and Nevis. A diagram summarising the key reorganisation steps involved is set out below for illustrative purposes:

A change of nationality and/or obtaining foreign identity by a famous PRC entrepreneur may attract considerable public attention. In addition, PRC individuals who habitually reside in the PRC for reason of economic interests may not simply oust the application of Circular 10 by obtaining foreign identities.

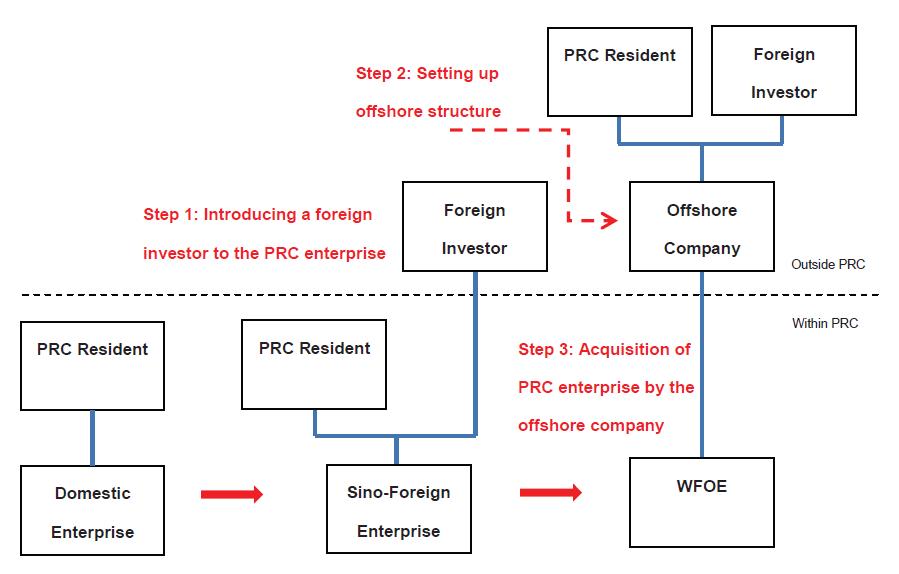

Introducing foreign investor(s)

While many successful listings have been achieved by the above-mentioned methods, these methods have their own shortcomings and limitations. In 2012, a breakthrough was achieved in the innovation of red chip listings, leading red chip listings into a new era.

In the listing of China Zhongsheng Resources Holdings Limited (Stock Code: 2623) in 2012, the red chip structure was developed by introducing a foreign investor to the relevant PRC domestic enterprise, thereby transforming the domestic enterprise into a Sino-foreign enterprise and subsequently a WFOE. As this enterprise only commenced the building of its red chip structure in 2010, that is, after the implementation date of Circular 10, its successful listing is said to have turned Circular 10 into a paper tiger[1]. A similar approach was adopted in the listing of China Tianrui Group Cement Company Limited (Stock Code: 1252).

A diagram summarising the key reorganisation steps involved in these cases is set out below for illustrative purposes:

After the listing of China Zhongsheng Resources Holdings Limited, it was originally perceived that the foreign investor concerned should hold at least 25% of the equity interest of the relevant PRC enterprise so as to ensure that Circular 10 would not apply. However, it may not be easy to find investors who are interested in acquiring 25% of the business, nor are many PRC business owners willing to sell 25% equity of their business to third parties before their listings. In 2014, the listing of Jiashili Group Limited (Stock Code: 1285) (“Jiashili”) provided a solution to these problems.

In the reorganisation of Jiashili, a Singapore citizen serving as the foreign investor acquired, through a SPV, only 1% of the equity interest of the relevant PRC enterprise (“1% Acquisition”). The PRC enterprise was then transformed into a Sino-foreign joint venture with the ratio of foreign investment of less than 25%, and subsequently a WFOE. According to the prospectus of Jiashili, the local Ministry of Commerce (“MOFCOM”) has verbally confirmed that:

1. Article 11 of Circular 10 (that is, where a domestic company or enterprise, or a domestic natural person, through an overseas company established or controlled by it/him, acquires a domestic company which is related to or connected with it/him, approval from MOFCOM is required) shall not apply to the 1% Acquisition; and

2. after the 1% Acquisition, the PRC enterprise would be converted into a Sino-foreign joint venture and further acquisition of its equity interest should not be subject to Circular 10.

In light of these recent cases, domestic enterprises could achieve their offshore listings more easily.

[1] “Zhongsheng Resources Holdings - New Route for Red Chip Listing” (〈中盛資訊控股「紅籌」新路徑〉) published in the September 2012 issue of Capital Finance

For enquiries, please feel free to contact us at: |

E: cc@onc.hk T: (852) 2810 1212 19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong Kong |

Important: The law and procedure on this subject are very specialised and complicated. This article is just a very general outline for reference and cannot be relied upon as legal advice in any individual case. If any advice or assistance is needed, please contact our solicitors. |