Double Duty: Disclosure of Interest in Associated Corporation

Background

Under Part XV of the Securities and Futures Ordinance (“SFO”), it imposes duties to file disclosure of interest forms on substantial shareholders and directors and chief executives of a listed corporation. While a director or chief executive of a listed corporation who is interested in the shares of the listed corporation should disclose his interest under the Form 3A, such a director or chief executive, who is also a director or chief executive of and is interested in the share of an associated corporation of that listed corporation, should also disclose his interest in the associated corporation using a separate form named Form 3B.

Disclosure obligations

If a director has an interest in shares of an associated corporation of a Hong Kong listed corporation of which he is a director, he has to disclose all dealings even if he only has an interest or a short position in a small number of shares or debentures. Such interests must be disclosed in the Form 3B.

Deemed interests are also included as interests which include a controlled corporation, a discretionary trust, and a beneficiary of a trust etc. A corporation is a “controlled corporation” if you control, directly or indirectly, one-third or more of the voting power at general meetings of the corporation, or if the corporation or its directors are accustomed to act in accordance with your directions.

What is an “associated corporation”?

Under s. 308 of the SFO, the definition of associated corporation includes a corporation which is:

- a subsidiary or holding company of a listed corporation or a subsidiary of the listed corporation’s holding company; or

- a corporation in which the listed corporation is interested in more than 20% of the issued shares of any class of its share capital.

Schedule 1 of the SFO also defines what a “holding company” refers to, which is, any other corporation of which it is a subsidiary. Given its reliance on the term “subsidiary”, the definition of subsidiary should be examined. Schedule 1 of the SFO provides that a corporation is a subsidiary of another corporation if:

- the other corporation:

- controls the composition of its board of directors;

- controls more than half of its voting power at general meetings; or

- holds more than half of its issued share capital (which issued share capital excludes any part thereof which carries no right to participate beyond a specified amount on a distribution of either profits or capital); or

- it is a subsidiary of a corporation which is the other corporation’s subsidiary.

Case studies

In order to better exemplify the situations of which an interest in the associated corporation should be disclosed using the Form 3B, the case studies below are illustrated. These cases are limited to the time when they were listed on the Hong Kong Stock Exchange, and so, the time of when they disclosed their interests in the associated corporation of a corporation was limited to the time when such a corporation becomes a listed corporation.

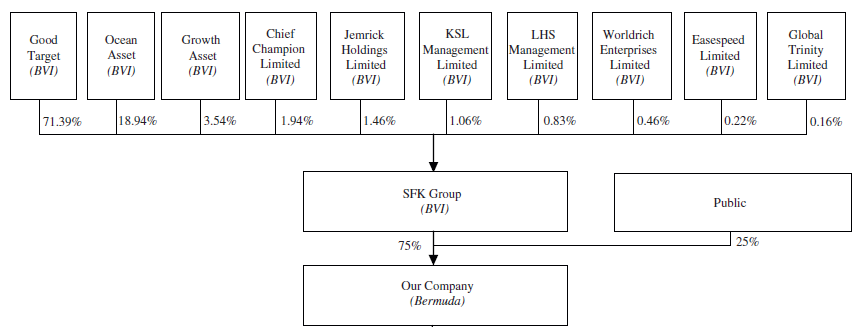

SFK Construction Holdings Limited

In the case of SFK Construction Holdings Limited, SFK Group owns more than 51% of its Listed Company, which means that the Listed Company is SFK Group’s subsidiary hence rendering SFK Group a holding company and therefore an associated corporation. In this present case, upon the listing of SFK Construction Holdings Limited, the director who also owns the entire issued share capital of Growth Asset, one of the parent companies of SFK Group, filed a Form 3B. Although Growth Asset is not a holding company of the Listed Company, the director of Growth Asset would have an interest in the shares of SFK Group under s. 344(3).

344(3) provides that a person is taken:

- to be interested in any shares in or debentures of the listed corporation or any associated corporation of the listed corporation in which a corporation is interested; and

- to have a short position in any shares in the listed corporation or any associated corporation of the listed corporation in which a corporation has a short position,

if:

- that corporation or its directors are accustomed or obliged to act in accordance with his directions or instructions; or

- he is entitled to exercise or control the exercise of one-third or more of the voting power at general meetings of that corporation.

And so, directors who fall under such provision are also required to file a Form 3B.

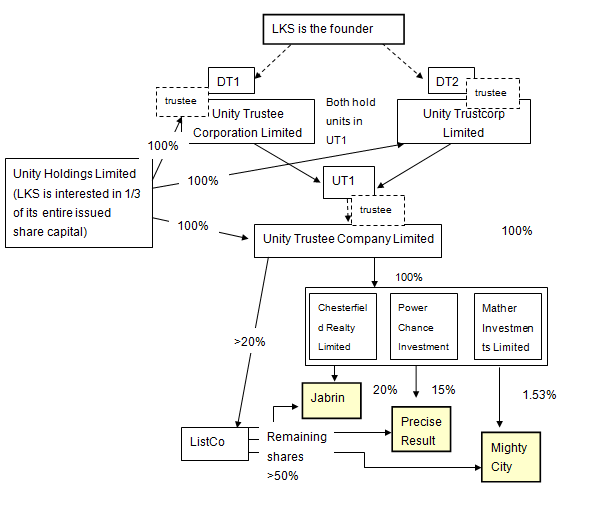

Cheung Kong Property Holdings Limited

After the listing of Cheung Kong Property Holdings Limited, Li Ka-shing filed three Forms 3B for three respective companies, namely Jabrin Limited, Precise Result Global Limited, and Mightycity Company Limited. These companies are subsidiaries of the Listed Company and their shares are held through the Unity Trustee Company Limited as a trustee of UT1. As the three companies which are wholly controlled by the Unity Trustee Company Limited would respectively have 20%, 15% and 1.53% of interest in the three companies, the Listed Company would own the remaining percentage of interest in those three companies. The three companies would therefore fall under the definition of subsidiaries of the Listed Company and are associated corporations.

Since Li Ka-shing is interested in one-third of the shares of Unity Holdings Limited, and that Unity Holdings Limited is interested in shares of the three companies, then its interest will be taken to be Li Ka-shing’s interest. However, since Unity Trustee Company Limited only holds interests as a trustee, Li Ka-shing is deemed to have interests in the three companies in the capacity of a founder. As discussed earlier, since deemed interests are also included as interests, it would stipulate the requirement of a Form 3B.

Conclusion

Although complicated, directors are required to disclose their interests in the associated corporation promptly. Non-disclosure or false or misleading disclosure would constitute as a criminal offence. For a first timer, a warning from the SFC would be appropriate if the aggregate value of the interests involved is less than HK$100,000. Nonetheless, timely and accurate disclosure is encouraged to be made accordingly in order to avoid any sorts of penalty.

For enquiries, please feel free to contact us at: |

E: cc@onc.hk T: (852) 2810 1212 19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong Kong |

Important: The law and procedure on this subject are very specialised and complicated. This article is just a very general outline for reference and cannot be relied upon as legal advice in any individual case. If any advice or assistance is needed, please contact our solicitors. |