Mandatory General Offer Obligation under the Takeovers Code

Introduction

On 22 November 2016, the Takeovers Executive of the Securities and Futures Commission (the “Takeovers Executive”) issued a decision to publicly censure and impose a 24-month cold-shoulder order against Mr Zheng Dunmu (“Mr Zheng”) for breaching the mandatory general offer obligation under Rule 26.1 of the Codes on Takeovers and Mergers and Share Buy-backs (the “Takeovers Code”).

Background

Mr Zheng is the founder of Changgang Dunxin Enterprise Company Limited (the “Changgang Dunxin”), which has been listed on the Main Board of the Hong Kong Stock Exchange since 26 June 2014. At the relevant times, Mr Zheng was also its controlling shareholder, the chairman and an executive director.

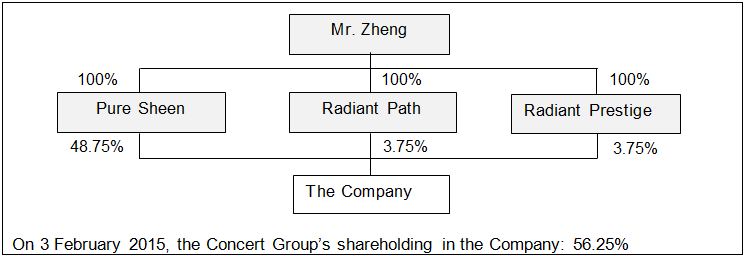

As at 3 February 2015, Mr Zheng was interested in 56.25% of Changgang Dunxin. These shares were held through three companies wholly-owned by Mr Zheng, namely Pure Sheen Limited, Radiant Path Limited and Radiant Prestige Limited as to 48.75%, 3.75% and 3.75% respectively. For the purposes of the Takeovers Code, Mr Zheng, Pure Sheen Limited, Radiant Path Limited and Radiant Prestige Limited are parties acting in concert (the “Concert Group”).

Relevant Transactions

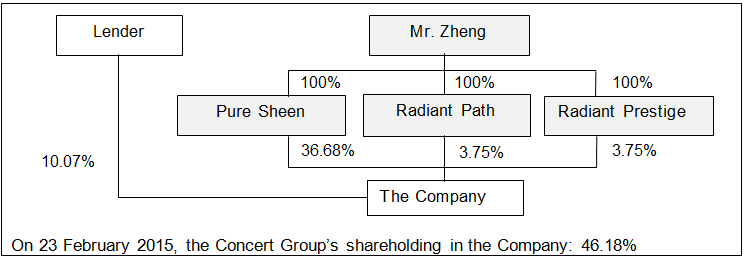

On 3 February 2015, Mr Zheng, on behalf of Pure Sheen Limited, entered into a stock secured financing arrangement with a third party (“Lender”) for a loan granted to Pure Sheen Limited. Pure Sheen Limited then pledged 10.07% of its interest in Changgang Dunxin as collateral for the loan. On 23 February 2015, the Lender sold the pledged securities, reducing the Concert Group’s interest in Changgang Dunxin from 56.25% to 46.18%.

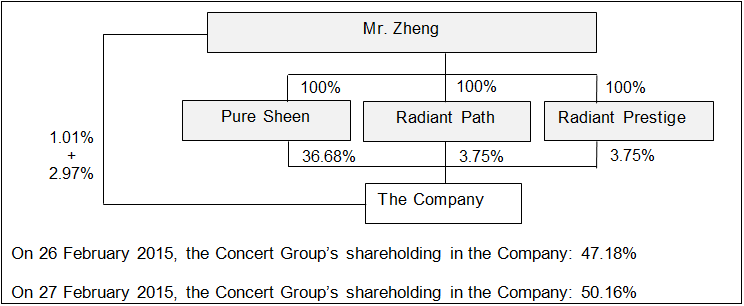

Shortly after becoming aware of the Lender’s disposals of the pledged securities, Mr Zheng personally acquired 1.01% and 2.97% of Changgang Dunxin on-market and off-market on 26 and 27 February 2015 respectively (“Acquisitions”). As a result of the Acquisitions, the Concert Group’s interest in Changgang Dunxin was increased from 46.18% to 50.16%, thereby crossing the 2% creeper threshold under Rule 26.1 of the Takeovers Code, triggering a mandatory general offer.

Upon becoming aware of the Acquisitions, the Takeovers Executive urged Mr Zheng to comply with the Takeovers Code by making a general offer to the shareholders of Changgang Dunxin. However, Mr Zheng confirmed, among other things, that he did not have sufficient financial resources to make a general offer for Changgang Dunxin in an announcement issued by Changgang Dunxin on 20 March 2015.

The “Creeper Provision”

Rule 26.1 of the Takeovers Code

According to Rule 26.1(d) of the Takeovers Code, subject to the granting of a waiver by the Executive, when two or more persons are acting in concert, and they collectively hold not less than 30%, but not more than 50%, of the voting rights of a company, and any one or more of them acquires additional voting rights and such acquisition has the effect of increasing their collective holding of voting rights of the company by more than 2% from the lowest collective percentage holding of such persons in the 12 month period ending on and inclusive of the date of the relevant acquisition, that person shall extend offers, on the basis set out in this Rule 26, to the holders of each class of equity share capital of the company, whether the class carries voting rights or not.

After the Lender’s disposal of the pledged securities, the Concert Group’s collective shareholding in Changgang Dunxin fell within the range of 30% to 50%. 46.18% became the Concert Group’s lowest percentage holding in Changgang Dunxin over the 12-month period before the Acquisitions. Following the Acquisitions, a mandatory general offer obligation was triggered on 27 February 2016.

Mr Zheng’s Arguments

Mr Zheng, while accepting that he has breached Rule 26.1(d) of the Takeovers Code and deprived Changgang Dunxin’s shareholders of the right to receive a general offer for their shares, submitted that he was misled into signing the financing agreement without proper legal advice and that the Lender disposed of the pledged securities wrongfully. Mr Zheng also informed the Takeovers Executive that he was not aware of the general offer obligation under the Takeovers Code at the time of the Acquisitions.

Takeovers Executive’s Ruling

The Takeovers Executive pinpointed that directors of a listed company should use the best of their abilities to comply with the Takeovers Code which may involve seeking professional advice as and when needed and, in some instances, consulting the Takeovers Executive prior to a course of action. Mr Zheng fell short of the standards expected of him and failed to seek advice or consult the Takeovers Executive before the Acquisitions.

Pursuant to sections 12.2(c) and 12.3 of the Introduction to the Takeovers Code, the Takeovers Executive imposed a cold-shoulder order against Mr Zheng, which is, a sanction denying him of direct or indirect access to the Hong Kong securities market for a period of 24 months commencing on 22 November 2016 to 21 November 2018.

Implications

Had Mr Zheng been aware of the relevant provisions under the Takeovers Code earlier, he could have applied for a Whitewash Waiver in accordance with the Takeovers Code, which would have availed him from the mandatory general offer obligation under Rule 26.1 of the Takeovers Code.

The Securities and Futures Commission strives to ensure protection of investors in Hong Kong’s securities markets. Practitioners and parties who wish to take advantage of the securities markets in Hong Kong shall conduct themselves in matters relating to takeovers, mergers and share buy-backs in accordance with the Takeovers Code. Otherwise, such practitioners and parties may find by way of sanction.

For enquiries, please contact our Corporate & Commercial Department:

E: cc@onc.hk

T: (852) 2810 1212

W: www.onc.hk

F: (852) 2804 6311

19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong Kong

Important: The law and procedure on this subject are very specialised and complicated. This article is just a very general outline for reference and cannot be relied upon as legal advice in any individual case. If any advice or assistance is needed, please contact our solicitors.